ProbCurve, and querying the resulting risk-neutral probability distribution. By the end you will have a working script you can adapt to any ticker.

1

Install

Install the library from PyPI. The standard install includes the built-in yfinance data connection used in this guide.

2

Fetch data

Import the modules you need, then use

sources.list_expiry_dates to see every available expiry for your ticker. Pass one of those dates to sources.fetch_chain to download the options chain and a market snapshot at the moment of download.chain contains the full options chain (calls and puts, strikes, bid/ask, open interest). snapshot captures the underlying price and the timestamp of the download — both of which you need in the next step.3

MarketInputs

MarketInputs bundles the three pieces of market context that OIPD needs to fit the model: the valuation date, the underlying price, and the risk-free rate. Pull the first two directly from the snapshot you just downloaded.4

Fit

Pass The returned

chain and market to ProbCurve.from_chain. This single call fits the SVI implied volatility smile and derives the risk-neutral probability distribution in one step.prob object is fully fitted and immediately queryable. No separate .fit() call is needed when using the from_chain factory.5

Query

Use the query methods on the fitted

ProbCurve to extract the statistics you care about.6

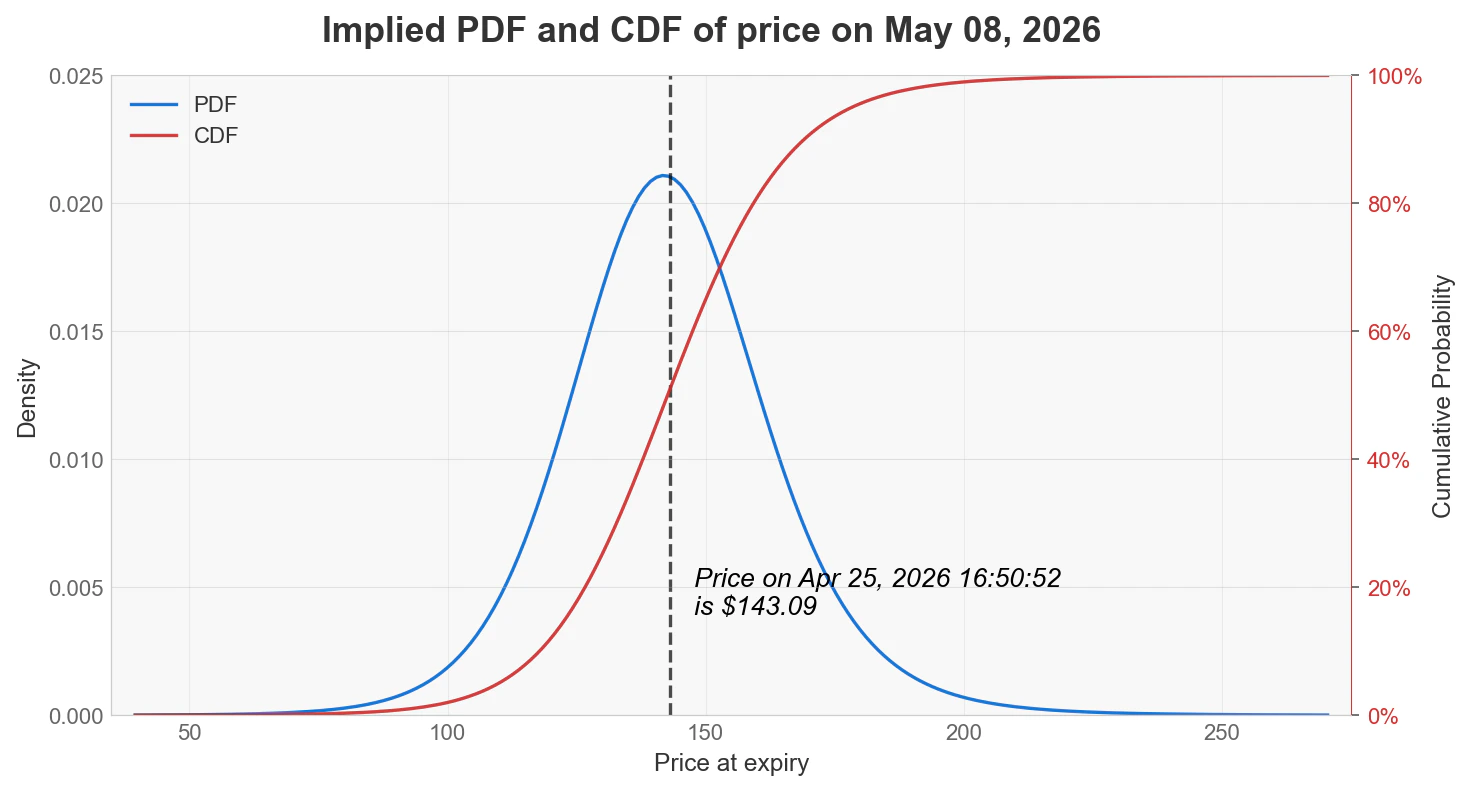

Plot

Call To save the chart instead:Example output:

prob.plot() to render the probability distribution as a chart. It returns a Matplotlib Figure, so you can save it or customise it with standard Matplotlib calls.This example uses live option data, so your chart will differ as prices, expiries, and spreads update.

Complete script

Here is the full example in one block, ready to copy and run:Next steps

Probability surface

Fetch a multi-expiry chain with

sources.fetch_chain(..., horizon="12m"), then pass it to ProbSurface.from_chain.Volatility smile

Work directly with

VolCurve and VolSurface to evaluate implied vols, price options, and compute Greeks.Data sources

Load data from a CSV or Pandas DataFrame instead of yfinance for corporate or internal data environments.

Warnings

Understand how OIPD surfaces data quality and model risk issues through structured diagnostics on every fitted object.